Professional Tips on Navigating Equity Release Mortgages

Professional Tips on Navigating Equity Release Mortgages

Blog Article

The Important Variables to Take Into Consideration Prior To Looking For Equity Release Mortgages

Before making an application for equity Release home loans, people must carefully think about several essential elements. Understanding the effects on their economic circumstance is important. This includes evaluating existing earnings, possible future expenditures, and the influence on inheritance. Additionally, checking out numerous item types and linked costs is essential. As one browses these complexities, it is necessary to weigh emotional connections to property versus practical economic requirements. What various other considerations might affect this substantial choice?

Recognizing Equity Release: What It Is and Exactly how It Works

Equity Release allows property owners, usually those aged 55 and over, to access the riches locked up in their property without needing to offer it. This economic solution makes it possible for people to disclose a part of their home's worth, giving money that can be utilized for numerous objectives, such as home renovations, debt payment, or boosting retirement revenue. There are two major kinds of equity Release products: lifetime home loans and home reversion strategies. With a lifetime mortgage, home owners keep ownership while obtaining against the building, paying off the financing and rate of interest upon fatality or relocating right into long-term care. On the other hand, home reversion involves offering a share of the building for a lump amount, permitting the house owner to remain in the home up until fatality. It is important for possible candidates to recognize the implications of equity Release, including the influence on inheritance and potential fees connected with the arrangements.

Examining Your Financial Circumstance and Future Demands

How can a homeowner properly assess their monetary circumstance and future demands prior to considering equity Release? They should conduct an extensive evaluation of their present earnings, costs, and cost savings. This includes reviewing monthly costs, existing financial debts, and any kind of possible earnings sources, such as pensions or investments. Recognizing capital can highlight whether equity Release is necessary for financial stability.Next, homeowners must consider their future demands. This entails expecting prospective healthcare expenses, way of life changes, and any significant costs that might emerge in retired life. Establishing a clear spending plan can help in determining just how much equity might be needed.Additionally, speaking with an economic consultant can offer insights right into the long-lasting effects of equity Release. They can assist in straightening the house owner's monetary situation with their future purposes, guaranteeing that any choice made is informed and straightened with their overall economic wellness.

The Impact on Inheritance and Family Members Financial Resources

The decision to make use of equity Release home mortgages can significantly affect household finances and inheritance planning. People should take into consideration the ramifications of estate tax and exactly how equity circulation among successors may alter as an outcome. These elements can influence not just the financial heritage left but additionally the relationships among household participants.

Inheritance Tax Obligation Effects

Lots of house owners consider equity Release home loans as a method to supplement retired life revenue, they might inadvertently affect inheritance tax liabilities, which can significantly affect household funds. When home owners Release equity from their residential property, the amount obtained plus interest builds up, reducing the worth of the estate left to beneficiaries. If the estate surpasses the tax obligation threshold, this can result in a higher inheritance tax costs. In addition, any type of staying equity might be considered as part of the estate, making complex the financial landscape for beneficiaries. Family members have to realize that the choice to accessibility equity can have long-term repercussions, possibly decreasing the inheritance intended for loved ones. As a result, mindful consideration of the ramifications is essential before continuing with equity Release.

Family Financial Planning

While thinking about equity Release home mortgages, households must identify the considerable impact these economic decisions can carry inheritance and general family finances. By accessing home equity, home owners might decrease the worth of their estate, possibly affecting the inheritance delegated heirs. This can cause sensations of uncertainty or problem among member of the family regarding future monetary expectations. Furthermore, the costs connected with equity Release, such as rates of interest and fees, can build up, reducing the staying assets offered for inheritance. It is vital for families to take part in open discussions about these problems, guaranteeing that all participants recognize the effects of equity Release on their long-lasting monetary landscape. Thoughtful preparation is vital to stabilize prompt financial requirements with future family members heritages.

Equity Distribution Among Successors

Equity circulation amongst successors can considerably alter the monetary landscape of a household, specifically when equity Release mortgages are included. When a homeowner chooses to Release equity, the funds drawn out might lessen the estate's overall value, impacting what heirs obtain. This reduction can result in conflicts amongst member of the family, specifically if assumptions regarding inheritance vary. The commitments linked to the equity Release, such as settlement terms and rate of interest build-up, can complicate monetary preparation for beneficiaries. Families need to consider how these elements affect their lasting financial health and connections. Seminar about equity Release choices and their effects can help ensure a more clear understanding of inheritance characteristics and mitigate prospective disputes amongst successors.

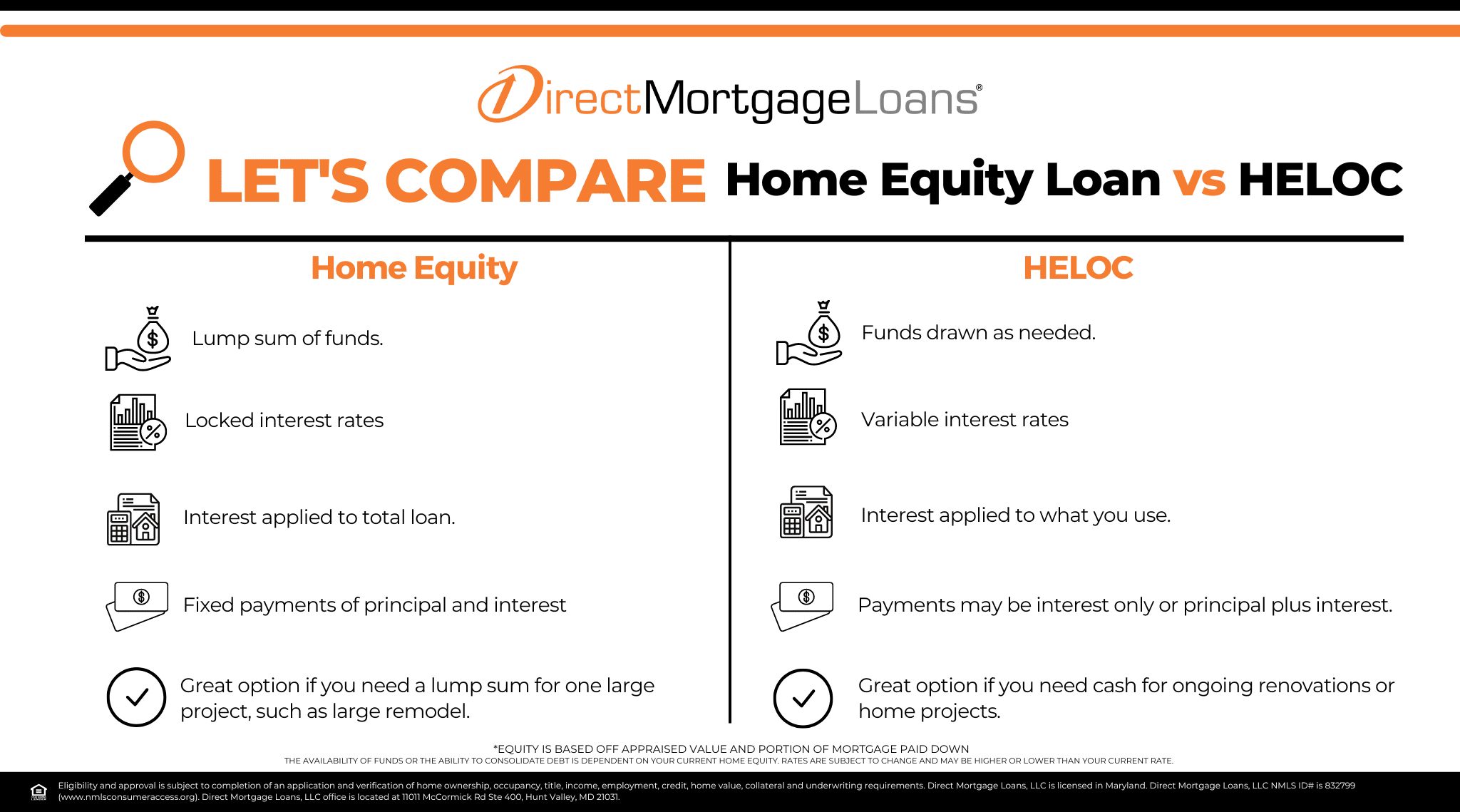

Exploring Different Kinds of Equity Release Products

When taking into consideration equity Release choices, people can select from several unique items, each tailored to different monetary demands and circumstances. The most common types include lifetime home mortgages and home reversion plans.Lifetime home mortgages allow property owners to borrow versus their building value while preserving ownership. The finance, along with built up interest, is settled upon the house owner's death or when they relocate into lasting care.In contrast, home reversion plans include selling a section of the home to a provider for a lump sum or regular repayments. The property owner can continue staying in the property rent-free until death or relocation.Additionally, some items provide adaptable functions, allowing borrowers to take out funds as needed. Each product lugs one-of-a-kind benefits and considerations, making it necessary for individuals to analyze their economic objectives and long-lasting effects before picking the most ideal equity Release option.

The Duty of Interest Rates and Fees

Picking the best equity Release item involves an understanding of various monetary elements, including rates of interest and connected charges. Passion rates can significantly influence the overall expense of the equity Release plan, as they identify exactly how much the borrower will owe gradually. Taken care of prices supply predictability, while variable rates can fluctuate, affecting long-lasting monetary planning.Additionally, consumers ought to know any kind of ahead of time costs, such as plan or appraisal charges, which can include to the initial price of the home mortgage. Ongoing fees, consisting of annual management charges, can also build up over the regard to the loan, potentially reducing the equity available in the property.Understanding these expenses is necessary for consumers to review the complete economic dedication and Go Here assure the equity Release item straightens with their economic objectives. Mindful factor to consider of rates of interest and charges can help individuals make educated choices that fit their scenarios.

Looking For Expert Guidance: Why It is necessary

Exactly how can individuals browse the intricacies of equity Release home loans successfully? Looking for expert guidance is a crucial step in this process. Financial experts and home loan brokers possess specialized knowledge that can brighten the details of go to these guys equity Release products. They can supply tailored assistance based on a person's distinct financial circumstance, making certain notified decision-making. Experts can help make clear conditions and terms, determine prospective risks, and highlight the long-lasting ramifications of getting in right into an equity Release contract. Furthermore, they can help in comparing numerous choices, making certain that people choose a strategy that lines up with their objectives and demands.

Examining Alternatives to Equity Release Mortgages

When taking into consideration equity Release home loans, people may locate it helpful to check out other funding choices that could much better fit their needs. This includes assessing the capacity of scaling down to access resources while preserving monetary security. A complete evaluation of these choices can bring about even more educated decisions pertaining to one's financial future.

Other Funding Options

Downsizing Considerations

Downsizing presents a sensible alternative for individuals considering equity Release mortgages, especially for those wanting to access the worth of their residential or commercial property without sustaining additional financial obligation. By marketing their present home and buying a smaller, extra budget-friendly home, home owners can Release substantial equity while decreasing living costs. This alternative not just minimizes financial problems however likewise simplifies maintenance responsibilities connected with larger homes. In addition, downsizing may provide an opportunity to relocate to an extra preferable location or a community tailored to their lifestyle requires. It is important for individuals to assess the emotional elements of leaving a long-time house, as well as the prospective costs included in moving. Mindful factor to consider of these aspects can lead to a more satisfying economic decision.

Frequently Asked Inquiries

Can I Still Move Home After Taking Out Equity Release?

The person can still relocate home after obtaining equity Release, but they have to ensure the new residential property meets the lender's requirements (equity release mortgages). Additionally, they see it here may require to repay the funding upon relocating

What Happens if My Building Value Reduces?

If a residential property's value lowers after obtaining equity Release, the homeowner may encounter decreased equity. Nonetheless, numerous strategies supply a no-negative-equity assurance, making certain that payment quantities do not go beyond the residential property's worth at sale.

Are There Age Restrictions for Equity Release Applicants?

Age restrictions for equity Release candidates typically require individuals to be a minimum of 55 or 60 years old, depending on the provider. These requirements guarantee that candidates are most likely to have adequate equity in their building.

Will Equity Release Affect My Qualification for State Conveniences?

Equity Release can possibly impact qualification for state benefits, as the launched funds might be considered revenue or capital (equity release mortgages). Individuals ought to consult financial advisors to understand exactly how equity Release influences their details benefit entitlements

Can I Pay Back the Equity Release Mortgage Early Without Penalties?

Final thought

In recap, maneuvering through the complexities of equity Release home mortgages calls for cautious factor to consider of numerous factors, including monetary circumstances, future demands, and the possible effect on inheritance. Understanding the different product choices, associated costs, and the relevance of specialist support is vital for making notified decisions. By extensively examining options and balancing psychological accessories to one's home with practical economic needs, people can figure out the most suitable method to accessing their home equity responsibly (equity release mortgages). Developing a clear spending plan can help in establishing just how much equity might be needed.Additionally, seeking advice from with a monetary consultant can offer insights right into the long-lasting ramifications of equity Release. Equity distribution among heirs can greatly alter the economic landscape of a family, particularly when equity Release home mortgages are entailed. Recurring costs, including annual monitoring costs, can likewise collect over the term of the lending, potentially minimizing the equity available in the property.Understanding these expenses is important for borrowers to review the total economic dedication and ensure the equity Release product aligns with their monetary objectives. If a residential or commercial property's worth reduces after taking out equity Release, the home owner may deal with lowered equity. Equity Release can potentially affect eligibility for state advantages, as the launched funds might be considered income or resources

Report this page